Wealth Defence

73% of high-net-worth families lose 25%+ in major life transitions.

A business sale. A health event. A partner exit. Retirement.

Without a coordinated strategy, the gap shows up too late.

The Problem

Your clients have great advisors — each doing their job under a different mandate. But no one is building a strategy that connects all of them.

You see the Gaps, but filling them isn’t your role

By the time a transition forces the issue, it’s too late to fix what wasn’t built

4–6

Advisors typically serving a business owner — each with a different mandate, none coordinating strategy.

Each advisor operates under a different mandate. Accountants own tax. Lawyers own documents. You own your piece. Nobody owns the whole picture. That’s the Transition Gap — and it only shows up when it’s too late.

Who We Are

How to give your clients complete wealth protection — without stepping outside your lane

We don’t replace your client’s existing advisors. We connect them — building one coordinated Wealth Defence strategy that makes every piece of their plan work together.

Our lane

Coordinated strategy across all advisors, documents, and structures

Your lane

Your relationship and expertise — completely unchanged

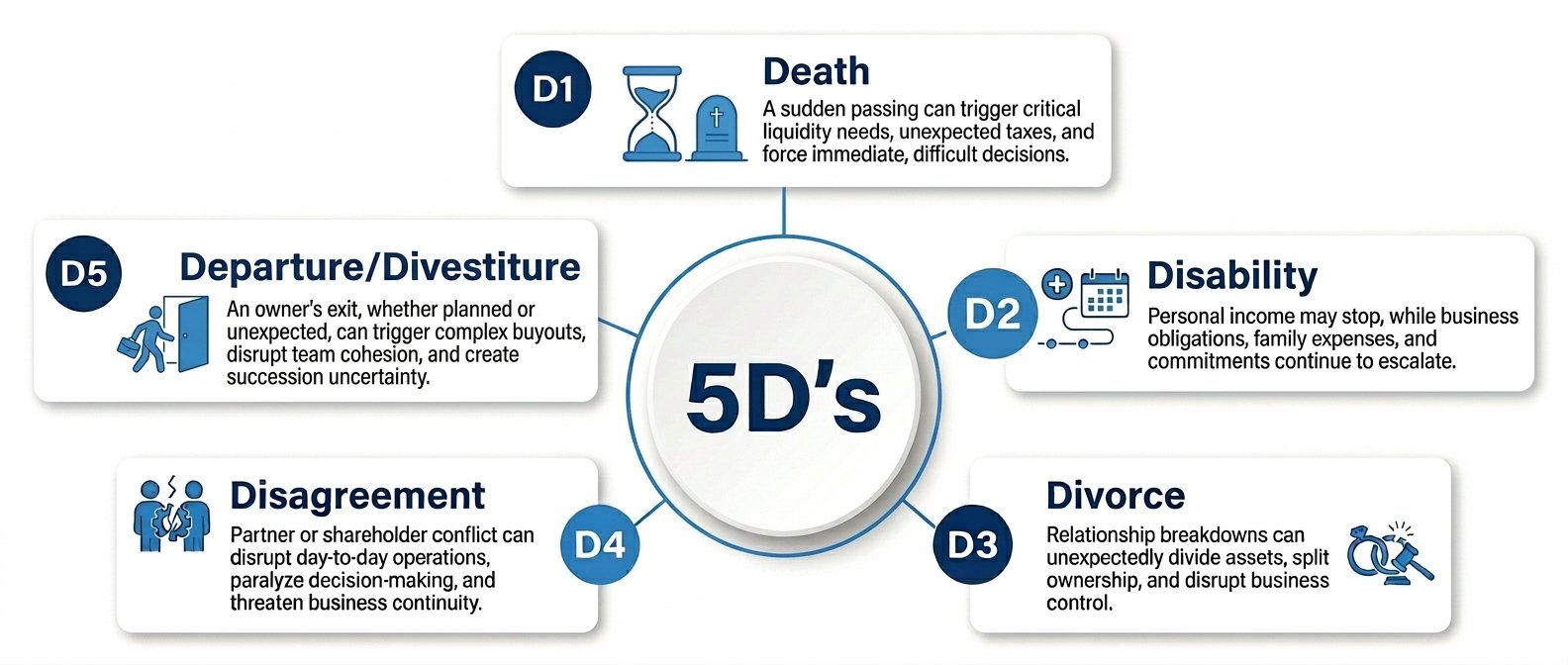

The 5 D's

The reason to act now — not react later

These aren’t triggers to wait for. By the time one of these hits, it’s too late to build what should have already been there.

The referral doesn’t happen when one of these hits. It happens before — so your client never has to find out what it costs to be unprepared.

Your client's silent partner — Tax (Ontario)

What Ottawa takes before your client sees a dollar

Your client has built significant wealth. But without a coordinated plan, Ottawa is already the largest shareholder in everything they own.

Why this matters to you as a referring partner: When your client transitions — through a sale, retirement, or estate — the tax hit across these asset classes compounds fast. Our role is to reduce that exposure before the event, not scramble after it.

Client keeps

Ottawa takes

Registered Assets

RRSP, RRIF, Pensions

$464,700

$535,300 gone

Client keeps 46%

53.5% taxed on withdrawal

Corporate Holdings

Retained earnings, Cash

Trapped inside corp

47%+ to move out

Not personal wealth until structured

47%+ on withdrawal or at estate

Capital Gains

Shares, Real Estate

$730,000

$270,000 gone

Client keeps 73%

27% taxed on disposition

Corporate Passive Income

Investment inside your corp

$498,300

$501,700

Client keeps 49.83%

50.17% tax on passive income within a corporation

$0

is what families pay in unnecessary tax — when the right structure is in place before the transition happens.

Is my client a fit?

Your client is a referral when they check any of these boxes

Business owner

Planning a sale, succession, or retirement

Incorporated professional

Professionals who bill through a corporation — or who could benefit from incorporating

High net worth family

Multi-generational wealth, estate complexity, or cottage/property transfers

Wealth across multiple buckets

Corp, real estate, investments, and cash

No unified plan in place

Advisors not working from a shared strategy

$5M — $25M

Typical wealth range across cash, business interests, real estate, and investments

What We Do

A coordinated strategy built around what your client already has

We connect your client’s existing advisors, documents, and structures into one plan that actually defends their wealth. The work often involves tax mitigation, estate planning, and philanthropy—frequently leveraging tax-exempt life insurance—to ensure every advisor is aligned and intentions become outcomes.

Understand

Map the wealth built and the legacy intended

Coordinate

Layer a strategy into the existing plan and team

Defend

Ensure intentions become outcomes — not tax bills

Reduce Ottawa's share

Less unnecessary tax across every asset class

Move corporate wealth

Into personal hands — efficiently and intentionally. The Capital Dividend Account (CDA) allows certain corporate proceeds — including life insurance payouts — to flow to shareholders completely tax-free.

Less unnecessary tax across every asset class

Create liquidity

When it’s needed — not after a transition forces it

Integrate philanthropy

Directing wealth to purpose is a strategy, not just a values choice — and often the most tax-efficient decision available.

Philanthropy as strategy — not charity

Many clients assume wealth flows to heirs — or quietly to tax. A third path exists: directing it intentionally to causes that matter through structures that also reduce tax exposure. For high-net-worth clients, philanthropy isn’t a values add-on — it’s often the most tax-efficient decision available. Gift-in-Kind donations, Donor Advised Funds, and charitable giving strategies can be layered directly into a Wealth Defence plan.

Without a strategy, wealth has gaps. Wealth Defence closes them.

Make the connection

One intro. Your client gets the missing piece.

Don’t wait for a trigger moment. The best time to refer is before one of the 5 D’s forces the conversation.

returnonlife.ca

647 697 5022

647 697 5022